Good Friday evening to all of you here on r/stocks! I hope everyone on this sub made out pretty nicely in the market this past week, and are ready for the new trading week ahead. 🙂

Here is everything you need to know to get you ready for the trading week beginning March 14th, 2022.

Federal Reserve expected to raise interest rates in week ahead, as Ukraine crisis adds volatility – (Source)

Federal Reserve Chair Jerome Powell testifies before Congress in the week ahead, and markets will hang on what he says regarding how the Russia-Ukraine conflict could affect Fed policy.

Investors may take the Federal Reserve’s first post-pandemic interest rate hike in stride, while uncertainty over the Ukraine crisis continues to hang over markets.

The Fed has clearly broadcast that it intends to raise its target fed funds rate by a quarter percentage point from zero, and it is expected to announce that move at the end of its two-day meeting Wednesday. The central bank should also reveal new forecasts for interest rates, inflation and the economy.

There are a few economic reports of note in the week ahead, including the producer price index Tuesday, retail sales Wednesday and existing home sales Friday.

“Earnings are over. Monetary policy is obviously going to be important here. I don’t see the Fed surprising anyone next week,” said Steve Massocca, managing director at Wedbush Securities. “It’s going to be a quarter point and then step into the background and watch what’s happening in Europe.”

Stocks fell for the past week, with the Nasdaq Composite the worst performer with a 3.5% decline. Meanwhile, the small-cap Russell 2000, which outperformed the three major indexes, lost 1% for the week.

A surge in oil prices spooked investors, with crude spiking to $130 at the beginning of the week but trading back below $110 on Friday.

The S&P 500 was down about 2.9% for the week. Energy stocks were the top performers, up nearly 1.9% and the only positive major sector.

Fed ahead

The impact of Russian sanctions on commodities markets and the lack of clarity around the outcome of the war in Ukraine are likely to keep volatility high across the financial markets.

The central bank’s statement and comments from Federal Reserve Chairman Jerome Powell on Wednesday will be closely watched for guidance on how Fed officials view the Ukraine crisis, and how much it could affect their outlook and the path for interest rates.

“His guidance is probably not going to be all that different from what he had to say in the [Congressional] testimony. Basically, downside risks to the growth outlook have increased. Upside risks to inflation have risen,” said Mark Cabana, head of U.S. short rates strategy at Bank of America.

Because Russia is a giant commodities producer, its assault on Ukraine and resulting sanctions have set off a rally in commodities markets that has made already-scorching inflation even hotter. February’s consumer price index was up 7.9%, and economists said rising gasoline prices could send it above 9% in March.

Gasoline at the pump jumped nearly 50 cents in the past week to $4.33 per gallon of unleaded, according to AAA.

Market pros see surging inflation as a catalyst that will keep the Fed on track to raise interest rates. However, uncertainty about the economic outlook could also mean the central bank might not hike as much as the seven rate increases that some economists forecast for this year.

Cabana expects Fed officials to forecast five hikes for 2022 and another four next year. The Fed previously anticipated three increases in both years. Cabana said the Fed could cut its forecast for 2024 to just one hike, from the two in their last outlook.

Any comments from the Fed on what it plans for its nearly $9 trillion balance sheet will also be important, since officials have said they would like to begin to scale it back this year after they start hiking interest rates. The Fed replaces maturing Treasury bonds and mortgages as they roll off, and it could slow that in a process Wall Street has dubbed “quantitative tightening” or QT.

“That they will be ready to flip the switch on QT in May is our base case, but we acknowledge there are risks that this will be skewed later,” said Cabana. He said if the Fed finds it is not in a position to raise interest rates as much as it hoped, it could delay shrinking the balance sheet right away, which would leave policy looser.

Bond market liquidity

The 10-year Treasury yield topped 2% at its highest level Friday, after dipping below 1.7% earlier this month as investors sought safety in bonds. Bond yields move opposite price.

“It’s inflation and inflation expectations. Treasurys behave in this environment a little differently than a flight to quality asset,” Cabana said “That’s a different dynamic than we’ve observed. You may see a flight to quality into Treasurys, but the Treasurys are reflecting higher inflation expectations.”

Cabana said the markets are showing signs of concern around the uncertainty in Ukraine. For instance, the Treasury market is less liquid.

“We have seen that the Treasury market has become more volatile. We’re seeing bid-ask spreads have widened. Some of the more traditionally less liquid parts of the market may have become less liquid, like TIPS and the 20-year. We’re also seeing market depth thinning out,” he said. “This is all due to elevated uncertainty and lack of risk-taking willingness by market participants, and I think that should worry the Fed.”

But Cabana said markets are not showing major stress.

“We’re not seeing signs the wheels are falling off in funding or that counterparty credit risks are super elevated. But the signs there are very much that all is not well,” he said.

“The other thing we continue to watch loosely are funding markets, and those funding markets are showing a real premium for dollars. Folks are paying up a lot to get dollars in a way they haven’t since Covid,” he said.

Cabana said the market is looking for reassurance from the Fed that it is watching the conflict in Ukraine.

“I think it would upset the market if the Fed reflected a very high degree of confidence in one direction or another,” he said. “That seems very unlikely.”

Dollar strength

The dollar index was up 0.6% on the week and it has been rising during Russia’s attack on Ukraine. The index is the value of the dollar against a basket of currencies and is heavily weighted toward the euro.

Marc Chandler, chief market strategist at Bannockburn Global Forex, also points out that the dollar funding market is seeing some pressure but it is not strained.

“The dollar is at five-year highs today against the yen. That’s not what you would expect in a risk-off environment,” he said. “That’s a testament to the dollar’s strength.”

Chandler said it’s possible the dollar weakens in the coming week if it follows its usual interest rate hike playbook.

“I think there might be a buy the rumor, sell the fact on the Fed,” he said. “That’s typical for the dollar to go up ahead of the rate hike and sell off afterwards.”

Oil on the boil

Oil gyrated wildly this past week, touching a high not seen since 2008, as the market worried there would not be enough oil supply due to sanctions on Russia. Buyers have shunned Moscow’s oil for fear of running afoul of financial sanctions, and the U.S. said it would ban purchases of Russian oil.

West Texas Intermediate crude futures jumped to $130.50 per barrel at the beginning of the week but settling Friday at $109.33.

“I think the market getting bid up to $130 was a little premature,” said Helima Croft, head of global commodities strategy at RBC, noting the U.S. ban on Russian oil. She said the run-up in prices Monday came as market players speculated there would be a broader embargo on Russian oil, including Europe, its main customer.

“Right now, the market is too extreme in either way. I think it’s justified at $110. I think it’s justified over $100. I don’t think we’re headed for an off-ramp, and I think we have room to go higher,” she said.

This past week saw the following moves in the S&P:

(CLICK HERE FOR THE FULL S&P TREE MAP FOR THE PAST WEEK!)

{kind=link}

S&P Sectors for this past week:

(CLICK HERE FOR THE S&P SECTORS FOR THE PAST WEEK!)

{kind=link}

Major Indices for this past week:

(CLICK HERE FOR THE MAJOR INDICES FOR THE PAST WEEK!)

{kind=link}

Major Futures Markets as of Friday's close:

(CLICK HERE FOR THE MAJOR FUTURES INDICES AS OF FRIDAY!)

{kind=link}

Economic Calendar for the Week Ahead:

(CLICK HERE FOR THE FULL ECONOMIC CALENDAR FOR THE WEEK AHEAD!)

{kind=link}

Percentage Changes for the Major Indices, WTD, MTD, QTD, YTD as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

S&P Sectors for the Past Week:

(CLICK HERE FOR THE CHART!)

{kind=link}

Major Indices Pullback/Correction Levels as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

Major Indices Rally Levels as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

Most Anticipated Earnings Releases for this week:

(CLICK HERE FOR THE CHART!)

{kind=link}

Here are the upcoming IPO's for this week:

(CLICK HERE FOR THE CHART!)

{kind=link}

Friday's Stock Analyst Upgrades & Downgrades:

(CLICK HERE FOR THE CHART LINK #1!)

{kind=link}

(CLICK HERE FOR THE CHART LINK #2!)

{kind=link}

(CLICK HERE FOR THE CHART LINK #3!)

{kind=link}

(CLICK HERE FOR THE CHART LINK #4!)

{kind=link}

Gas Prices Hit A New Record

Crude oil may have reversed lower this week, but it's hard to tell when drivers head to the pumps. The national average for a gallon of regular gasoline has continued to rise to hit a record high of $4.33 in data from AAA going back to 2004. While prices typically rise this time of year, the vertical move this year has meant prices have grown at a much more rapid rate than normal.

(CLICK HERE FOR THE CHART!)

{kind=link}

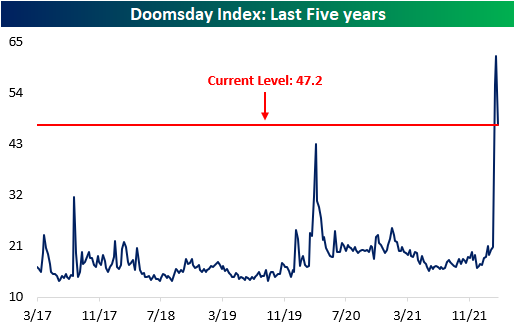

Doomsday Fear Index

During the Cold War, American children and adults were educated on how to best protect themselves from a nuclear explosion. This included measures from the silly “duck and cover” campaign to nuclear fallout shelter instructions. If you happen to be curious about the federal government's current recommendations in regards to protection from a nuclear blast, you can read up on the instructions here. We're not sure how focused people will be about wearing a mask in the event of nuclear fallout, but we guess you can never be too careful!

With tensions between Western nations and Russia reaching levels not seen since the Cold War, we took a look at Google Trends to identify the level of fear in the American population with respect to the current war in Ukraine. We looked at the search volumes for terms like nuclear war, WWIII, canned food, Potassium Iodide, and gas mask. Searches for many of these terms hit five-year highs in the early days of the Russian invasion but have subsided since. The current level is still well above normalcy, but fears appear to have eased over the last week as the West's retaliation has been almost entirely economic (or maybe there is no internet service in the fallout shelters). The aggregate index is pictured below.

(CLICK HERE FOR THE CHART!)

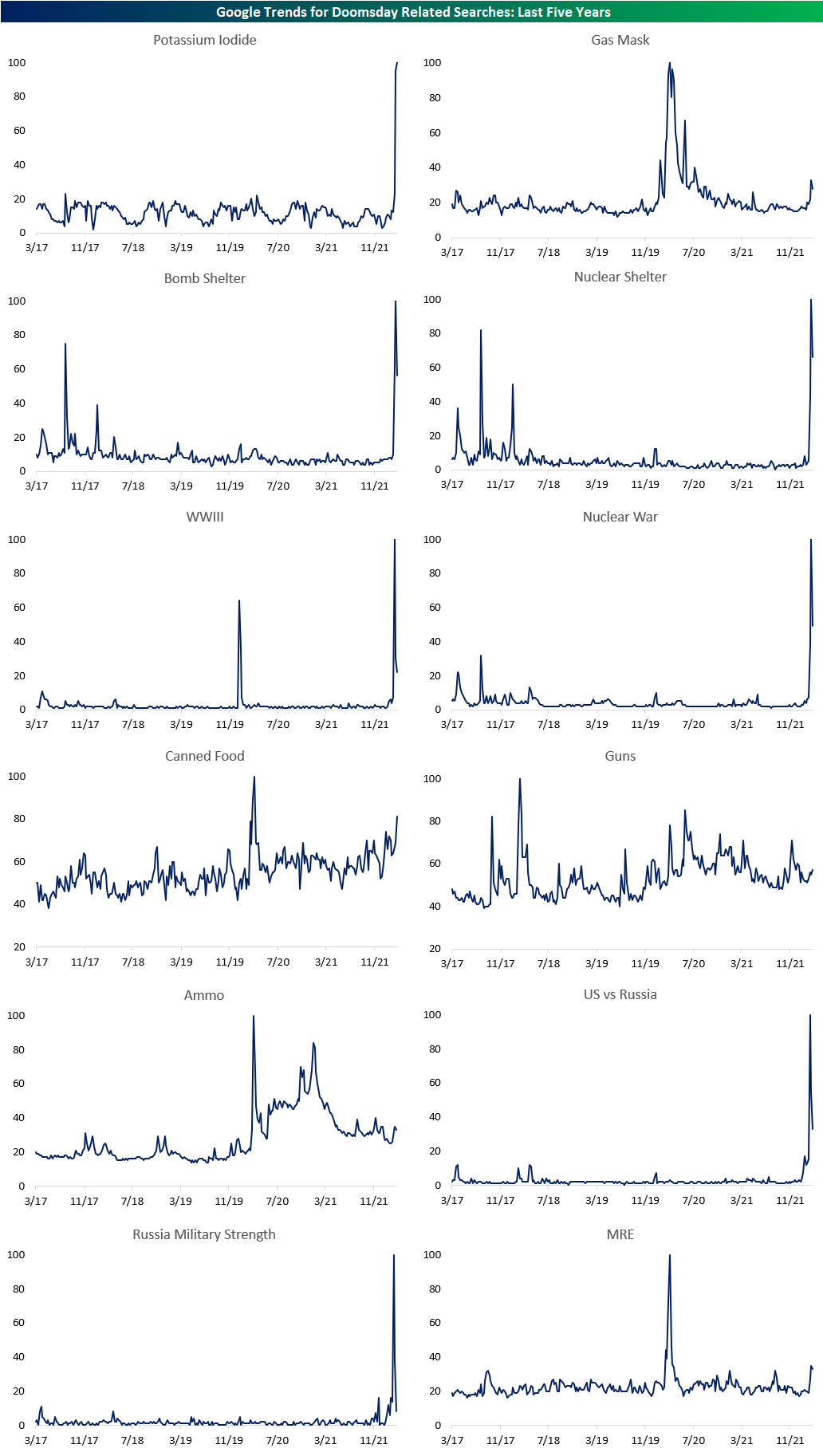

Below are charts of each search term we utilized in the composition of our index. Potassium Iodide, the compound utilized to mitigate the effects of excessive radiation exposure, is the only term that remains at a five-year high in terms of search volume. While searches for some of these terms were actually much higher during the early days of COVID, they all experienced upticks in the last few weeks. All-in-all, based on search trends based on fears of a nuclear situation or war with Russia spiked when the Ukraine invasion first started, but those fears have over the course of the last week.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

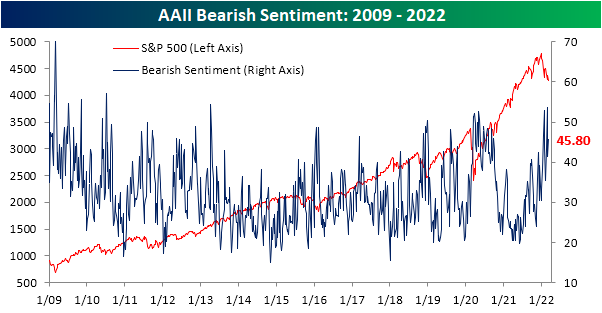

Investor Sentiment Remains Volatile

Considering equities and other risk asset prices continue to swing violently, so too have readings on investor sentiment. The weekly AAII survey of individual investors saw the percentage of respondents reporting as bullish fall back below 25% this week after rising above 30% last week. While that is not the largest drop in recent months (the second week of January saw bullish sentiment fall 7.9 percentage points compared to 6.4 today), it nonetheless reaffirmed that investor confidence is shaky, if not undecided, at the moment.

(CLICK HERE FOR THE CHART!)

The drop in bullish sentiment was mostly picked up by those reporting as bearish. Bearish sentiment rose 4.4 percentage points to 45.8%. While that reading is roughly 15 percentage points above the historical average for bearish sentiment, the reading is still lower than an even more pessimistic reading only two weeks ago when more than half of respondents reported as bearish.

(CLICK HERE FOR THE CHART!)

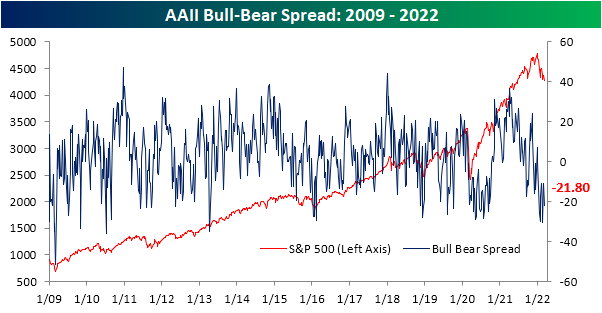

With the inverse moves in bullish and bearish sentiment, the bull-bear spread has pulled back to -21.8. As with bullish and bearish sentiment, even if that does not set a new low, it is only in the 5th percentile of readings going back to the start of the survey.

(CLICK HERE FOR THE CHART!)

After the largest single-week decline in nearly 20 years two weeks ago, neutral sentiment has been clawing its way back into the range it was in for most of the past year. Gaining another 2 percentage points this week, the reading is now back above 30%.

(CLICK HERE FOR THE CHART!)

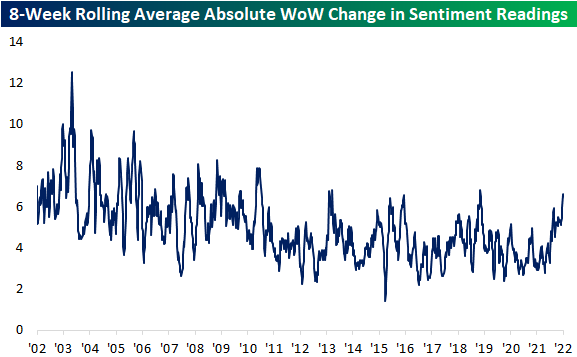

Across each category of the report, there have been sizable swings in the past two months. To highlight this, in the chart below we show the eight-week rolling average of the absolute week over week change for each sentiment reading (bullish, bearish, and neutral) over the past 20 years. Over the history of the survey, weekly changes have gravitated towards smaller swings meaning the past decade is structurally a bit different relative to the decade before that. That being said, the weekly swings in the AAII readings on sentiment have been some of the largest of any period of the post-Global Financial Criss era. In fact, not even the COVID crash saw such volatility in sentiment (given optimism collapsed and then remained muted for some time rather than swing back and forth) while the only times this average was as high as now in the past decade were the spring of 2013, February 2016, and January 2019.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

More Volatility Likely in March, Recent Lows Remain Key

Thus far the market has been unable to find any real traction in the historically bullish month of March. As of today’s close DJIA is down 3.72% in March. S&P 500 is off 4.65%, NASDAQ is fallen 6.95% while the Russell 2000 is lower by 4.15%. Today’s gain by the small-cap Russell 2000 is somewhat encouraging and adds to the accumulating evidence that the market may finally be coming to terms with Ukraine, inflation, and the Fed. As we have noted in recent posts, investor sentiment has reached bearish levels last seen at the start of the covid-19 pandemic, S&P 500 has held its intra-day low reached on February 24 and VIX, although elevated, has not exploded to full-blown panic levels.

In addition, we can add March’s typical performance over the last 21-years to this list. As you can see in the chart above, the market has tended to selloff early in March and find a bottom around the sixth trading day of the month. Today was the sixth trading day. Afterwards the trend remains choppy, but it is generally higher until the end of the month.

(CLICK HERE FOR THE CHART!)

{kind=link}

Be Greedy When Others Are Fearful

On this 13th Anniversary Global Financial Crisis Low, we may want to heed the wise words of one of the greatest investors of all time. “You try to be greedy when others are fearful, and fearful when others are greedy.” – Warren Buffett

So we ask: are we hitting another March market low on the 13th anniversary of the Global Financial Crisis low? It’s too early to be sure, but today’s rally and the recent dire projections and fearful sentiment are encouraging. CNN’s Fear & Greed Index shown above has clearly reached the extreme fear levels associated with market lows and turns.

Last week we posted how it was beginning to look like Investors Intelligence Bullish and Bearish Advisors % were indicating that contrary bearish sentiment was near bottoming levels. This may not be the final low, but the bottoming process is clearly underway. Sit tight and stick to your system.

(CLICK HERE FOR THE CHART!)

{kind=link}

Country ETFs Falling Below Pre-COVID Highs

Headed up to the two-year anniversary of the COVID crash low (3/23/20), equities around the globe have been experiencing some of the worst pullbacks since that period. In the table below, we show the country ETFs of the countries tracked in our Global Macro Dashboard as well as their year and month to date performance, performance since each respective 52-week high as of 2/19/20 (the S&P 500 and a handful of other global indices last high before entering bear markets during the COVID crash) and current 52-week high. We also show where they are currently trading with respect to their 50-DMAs.

Given the degree of declines recently, nearly everything is oversold with six countries' readings now 'off the chart' as they trade well over three standard deviations below their 50-DMAs. The average country ETF is also down double digits on both a YTD basis and relative to their respective 52-week highs. Of the countries shown below, only Brazil (EWZ) and South Africa (EZA) are higher YTD with gains of 17.56% and 9.27%, respectively. Russia (RSX), meanwhile, is obviously down the most having been cut by over 75%.

The average country ETF is now down over 20% from its 52-week high, and only four of those 52-week highs have come since the start of 2022 whereas most were set last spring. As for how the current drawdowns have eaten into the post-COVID rallies, below we also show the percent change of these ETFs relative to their 52-week highs as of 2/19/20. In other words, where each ETF is trading with respect to their pre-COVID highs. Currently, there are only 8 country ETFs that remain above their respective pre-COVID highs. Seven others, meanwhile, have now declined more than 20% below their pre-COVID highs. Of course, Russia is once again down the most dramatically from those levels falling more than 75%.

(CLICK HERE FOR THE CHART!)

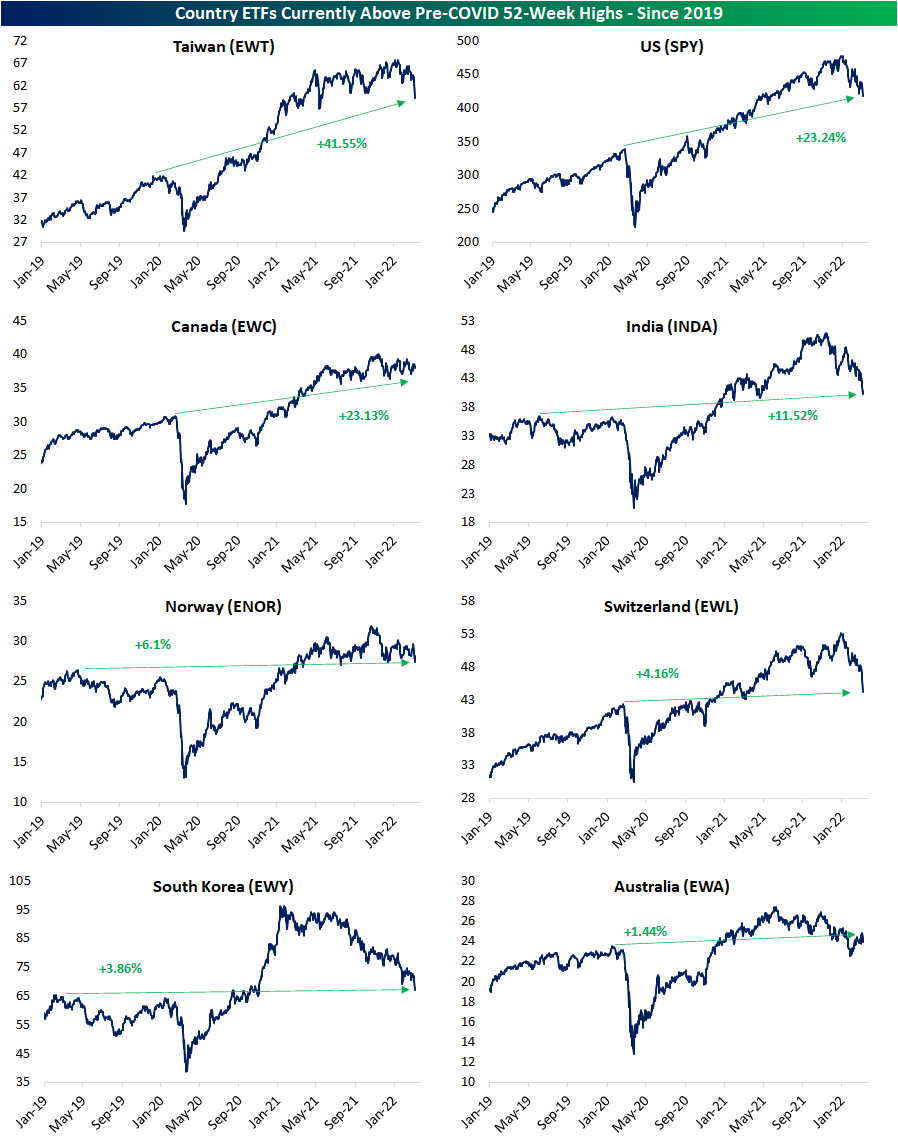

Below we show the charts of those eight countries that are currently still in the green relative to pre-COVID highs. The recent rough patch is not exactly identical for all countries though. Whereas the downtrends for some like Taiwan (EWT) or the US (SPY) are bringing these ETFs to multimonth lows, others like Canada (EWC) and Norway (ENOR) have more or less trended sideways. Since retaking pre-COVID highs, only Australia (EWA) has gone on to recently retest/fall back below those levels which it did in late January. While it would mean much further downside for the likes of EWT, SPY, and EWC, those prior highs could mark one area of tangible support for these other countries.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

The Little Guy Eying Inflation

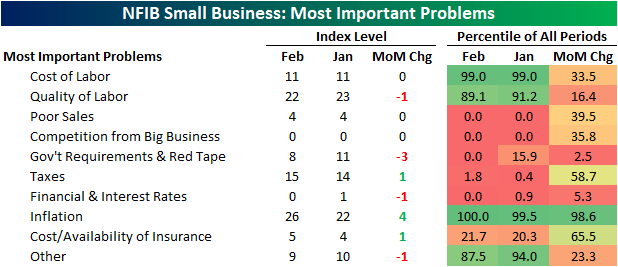

Looking across the range of issues surveyed by the NFIB, labor and inflation remain front and center of what most concerns small businesses. As shown below, the combined percentage of respondents reporting either cost or quality of labor as their most important problem continues to be the most prevalent topic with 33% of firms reporting as such. That is down slightly from 34% in January thanks to the decline in quality of labor. Most other categories fell to or remained at record lows. Such was the case for Poor Sales, Competition from Big Business, Government Requirements and Red Tape, and Financial & Interest Rates.

(CLICK HERE FOR THE CHART!)

Last month the percentage of respondents reporting inflation as their biggest problem went unchanged from the December reading of 22%. This month that reading gained another 4 percentage points to cross above a quarter of all respondents for the first time on record going back to 1986. Behind labor concerns (the combined reading of cost and quality of labor), this is the most commonly reported problem, and based on the action in commodities prices over the last couple of weeks, this reading will almost certainly increase again next month.

(CLICK HERE FOR THE CHART!)

That means what has usually been the second most important problem on a combined basis recently, government requirement and taxes, dropped in the ranking. In fact, the 3 percentage point decline in government requirements offset the one percentage point increase in taxes to tie the November 2005 reading for the lowest on record. As we have noted in the past, the past few presidential cycles have structurally seen lower readings in these indices when Republicans were in office and vice versa when Democrats have held the presidency. With Biden currently in office, the record low reading is somewhat unusual from this political perspective.

(CLICK HERE FOR THE CHART!)

That is not the only category that has fallen to record lows. Poor sales and competition from big business have both fallen dramatically in the past couple of years.

(CLICK HERE FOR THE CHART!)

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Here are the most notable companies reporting earnings in this upcoming trading week ahead-

(CLICK HERE FOR NEXT WEEK'S MOST NOTABLE EARNINGS RELEASES!)

(CLICK HERE FOR NEXT WEEK'S HIGHEST VOLATILITY EARNINGS RELEASES!)

{kind=link}

(CLICK HERE FOR THE NOTABLE EARNINGS BEFORE THE OPEN ON MONDAY!)

{kind=link}

Below are some of the notable companies coming out with earnings releases this upcoming trading week ahead which includes the date/time of release & consensus estimates courtesy of Earnings Whispers:

Monday 3.14.22 Before Market Open:

(CLICK HERE FOR MONDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Monday 3.14.22 After Market Close:

(CLICK HERE FOR MONDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK# 1!)

{kind=link}

{kind=link}

Tuesday 3.15.22 Before Market Open:

(CLICK HERE FOR TUESDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Tuesday 3.15.22 After Market Close:

(CLICK HERE FOR TUESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

{kind=link}

Wednesday 3.16.22 Before Market Open:

(CLICK HERE FOR WEDNESDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Wednesday 3.16.22 After Market Close:

(CLICK HERE FOR WEDNESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

{kind=link}

Thursday 3.17.22 Before Market Open:

(CLICK HERE FOR THURSDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Thursday 3.17.22 After Market Close:

(CLICK HERE FOR THURSDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

{kind=link}

Friday 3.18.22 Before Market Open:

(CLICK HERE FOR FRIDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK!)

{kind=link}

Friday 3.18.22 After Market Close:

([CLICK HERE FOR FRIDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

(NONE.)

DISCUSS!

What are you all watching for in this upcoming trading week?

(T.B.A. THIS WEEKEND.)

(T.B.A. THIS WEEKEND.) (T.B.A. THIS WEEKEND.).

(CLICK HERE FOR THE CHART!)

I hope you all have a wonderful weekend and a great trading week ahead r/stocks. 🙂

Leave a Reply