Good Friday evening to all of you here on r/stocks! I hope everyone on this sub made out pretty nicely in the market this past week, and are ready for the new trading week ahead. 🙂

Here is everything you need to know to get you ready for the trading week beginning March 28th, 2022.

Stocks could take their cue from oil, inflation and interest rates in the week ahead – (Source)

With the Federal Reserve’s first rate hike out of the way, market pros are now debating whether the market can continue the upswing it started in the past week.

March’s employment report is coming up in the week ahead, but developments in Ukraine, the price of oil and an inflation report are likely to steer the market.

Stocks notched gains for the week, while interest rates ripped higher and oil prices jumped. Energy was the top performing sector, up more than 7%, as West Texas Intermediate crude futures closed nearly 9% higher for the week. The closely-watched 10-year Treasury yield was on a tear, reaching 2.5% Friday, its highest level since May 2019 from 2.14% just a week earlier.

Traders are also watching the rise interest rates to see if they will stall the market’s gains. The S&P 500 was up nearly 1.8% for the week, ending Friday at 4,543.06.

“Since the war started, on the ten days that were up, the S&P 500 was up at least 1%,” said Art Hogan, chief market strategist at National Securities. “I don’t think next week is going to be any different. We’re going to be headline driven, whether it’s economic data, news out of Ukraine or crude oil futures.”

The market has chopped around but is higher for the month of March so far. The S&P was up nearly 3.9% for the month-to-date on Friday.

Katie Stockton, founder of Fairlead Strategies, said stock charts look promising for the near term but are less clear longer term.

“We should take advantage of this short-term momentum. I feel pretty good about it short-term. I mean several weeks,” she said. “We’ve also seen some nice short-term breakouts… names getting above their 50-day moving averages.”

She said 58% of the S&P 500 companies are now above their 50-day moving averages, a positive sign for momentum. The 50-day is simply the average closing price over the past 50 sessions, and a move above it can signal more upside.

Stocks like Tesla, Microsoft, Apple and Alphabet have all regained their 50-day moving averages, she said. Stockton noted that some high-growth tech names have also done so. She pointed to CLOU, the Global X Cloud Computing ETF.

As for yields, she said the 10-year looks set to consolidate now that it has touched 2.50%. Her next target is 2.55%. “If we get above 2.55%, the next hurdle is 3.25%,” she said.

Jobs and inflation

There is a busy economic calendar in the week ahead, highlighted by the March jobs report and personal consumption expenditures data.

Consumer confidence and home price data will be released Tuesday.

PCE includes an inflation measure that is closely watched by the Fed. Economists expect to see core PCE inflation up by 5.5% year-over-year when it is reported Thursday, according to Dow Jones.

There is also the ISM manufacturing survey reported Friday. The key nonfarm payrolls report will also run that day.

Economists expect 460,000 jobs were added in March and the unemployment rate fell to 3.7%, according to Dow Jones. That compares to the 678,000 nonfarm payrolls added in February and an unemployment rate of 3.8%.

“I definitely think at this point that inflation data is much more meaningful than employment, in terms of the path of the economy,” said Ben Jeffery, vice president of U.S. rates strategy at BMO. Jobs will still matter, but the Federal Reserve has pivoted to focus more on combating inflation, while the economy is reaching maximum employment.

Fed Chairman Jerome Powell made that point when he spoke to economists Monday, saying the central bank would be willing to be more aggressive raising interest rates to battle inflation. Stocks initially sold off on his comments, amid fears the Fed could slow the economy or even bring on a recession.

Since then, stocks moved higher, but interest rates have been galloping higher. The fed funds futures market has been pricing in 50-basis-point rate hikes — or 0.5% — in both May and June.

″[Nonfarm payrolls] will matter… I do think it’s probably going to be more a story of just how far the market is willing to press the 50-basis-point rate hike narrative, which is likely to be more pressing next week,” said Jeffery. “The excitement that once surrounded jobs is definitely less so at this point in the cycle.”

In the bond market, Jeffery said investors will be watching Treasury auctions Monday and Tuesday, when the government issues $151 billion in 2-year, 5-year and 7-year notes.

Rising oil prices have been driving inflation expectations higher, and the bond market is closely watching crude prices, as is the stock market. West Texas Intermediate crude futures settled up 8.8% for the week, at $113.90 per barrel Friday.

Oil heats up

“It seems like oil north of $100 has some staying power,” BMO’s Jeffery said.

Michael Arone, chief investment strategist at State Street Global Advisors, said the pattern between stocks and oil will continue to be important. When oil has spiked recently, stocks have weakened, he said. Meanwhile, when crude falls, stocks have been able to rally,

“It seems like this week it was a bit more pronounced again when oil prices were rising pretty aggressively,” Arone said. “It’s got this interconnectedness to a few things — sentiment about the Ukraine conflict, how’s that going, inflation and ultimately how hawkish or dovish the Fed is going to be. I think it’s emerged as one of those binary proxies for these other elements in the market.”

“It’s just a barometer for those other things — the Ukraine conflict, inflation and the Fed,” he said.

Arone said as investors anticipate some sort of resolution that will end the conflict in Ukraine, but it’s not clear when. “The headlines coming out of Ukraine will continue to cause volatility,” he said. “At the margin, investors are gaining comfort with the likely outcome.”

Arone said stock market fundamentals are better than some investors expect. When inflation rises, topline revenues can also go higher.

“Everyone knows multiples have contracted, stocks have gotten cheaper, but one thing that’s gotten lost on investors is top-line revenues have this correlation with inflation,” he said. “Corporate profits and CPI [the consumer price index] are kind of connected. You have multiples contracting but earnings estimates are rising.”

Arone said stocks are reasonably positioned and investors are getting more comfortable that there will be a favorable resolution to the war.

“If we can get past the Ukraine conflict and some of the fears about the Fed and inflation, I think the fundamentals are okay,” he said.

This past week saw the following moves in the S&P:

(CLICK HERE FOR THE FULL S&P TREE MAP FOR THE PAST WEEK!)

{kind=link}

S&P Sectors for this past week:

(CLICK HERE FOR THE S&P SECTORS FOR THE PAST WEEK!)

{kind=link}

Major Indices for this past week:

(CLICK HERE FOR THE MAJOR INDICES FOR THE PAST WEEK!)

{kind=link}

Major Futures Markets as of Friday's close:

(CLICK HERE FOR THE MAJOR FUTURES INDICES AS OF FRIDAY!)

{kind=link}

Economic Calendar for the Week Ahead:

(CLICK HERE FOR THE FULL ECONOMIC CALENDAR FOR THE WEEK AHEAD!)

{kind=link}

Percentage Changes for the Major Indices, WTD, MTD, QTD, YTD as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

S&P Sectors for the Past Week:

(CLICK HERE FOR THE CHART!)

{kind=link}

Major Indices Pullback/Correction Levels as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

Major Indices Rally Levels as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

Most Anticipated Earnings Releases for this week:

([CLICK HERE FOR THE CHART!]())

(T.B.A. THIS WEEKEND.)

Here are the upcoming IPO's for this week:

(CLICK HERE FOR THE CHART!)

{kind=link}

Friday's Stock Analyst Upgrades & Downgrades:

(CLICK HERE FOR THE CHART LINK #1!)

{kind=link}

(CLICK HERE FOR THE CHART LINK #2!)

{kind=link}

The Bull Market Turns Two

The bear market ended two years ago today and the subsequent bull market has clearly been an amazing ride. For some context, it was the fastest bull market to double ever, at just under 18 months.

(CLICK HERE FOR THE CHART!)

Here’s where it ranks against the other bull markets that have doubled. You can see it is currently up 102%, making it the best bull market on its second birthday ever. 2009 was up 95%, coming in second.

(CLICK HERE FOR THE CHART!)

At the recent peak in early January, the S&P 500 Index was up 114%, making it the seventh bull market to double. The annualized return of 53.4% shows just how explosive this move was off the lows and does imply some type of break could be warranted.

(CLICK HERE FOR THE CHART!)

Here’s another way to look at this bull market as it starts year three. Previous strong bull markets saw modest gains and really spent much of the third year consolidating the previous big gains.

(CLICK HERE FOR THE CHART!)

“As this bull market reaches the third year of life, investors need to remember that year three of bull markets tend to be a little tamer, with the larger gains happening in year one and two,” explained LPL Financial Chief Market Strategist Ryan Detrick. “In fact, out of the 11 bull markets since World War II, we found that three of them ended during year three, while the ones that didn’t end saw an average gain of only 5.2%.”

As shown in the LPL Chart of the Day, year three of bull markets have returned only 5.2% on average for the S&P 500, versus first year gains of 41.8% and second year gains of 12.8%, while three bull markets outright ended in year three.

(CLICK HERE FOR THE CHART!)

We expect the bull market to continue, but some bumps in the road are normal. As the bull ages, year three could provide some of those bumps.

For more on the bull market turning two and what could happen next, please watch the latest LPL Market Signals podcast with Jeff Buchbinder and Ryan Detrick, as they break it all down.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

5 Energy Stocks Reached ATHs

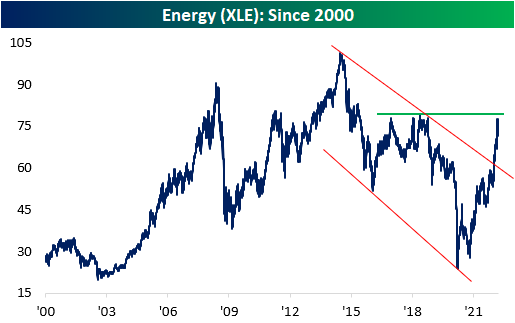

Energy stocks have roared higher since the beginning of 2022, gaining a whopping 38.8% in less than three months (as of yesterday's close). This comes on the back of sharp moves higher in crude, thus implying higher margins and increased bottom line earnings per share. During the pandemic, energy stocks were among the most hurt, as a reduction in travel and economic activity led to a crash in oil markets. Although the YTD gain is certainly substantial, investors that have held energy stocks since mid-2008 are still in the red. The energy sector ETF (XLE) is still 23.0% off of its high price since the turn of the century, which occurred in June of 2014. As you can see from the chart below, XLE has broken its long-term downtrend and is nearing a breakout above 2018 levels. To retest the high of the century, XLE would need to gain another 29.8%.

(CLICK HERE FOR THE CHART!)

On March 11th of this year, the relative strength reading of XLE vs the S&P 500 (SPY) since 2000 turned positive for the first time since COVID was declared a pandemic by the World Health Organization (WHO). The ratio has since turned negative, and the reading is currently -5.0 percentage points. The relative strength had moved continuously lower from its high in 2008 through early 2021, but the recent reversal higher is substantial.

(CLICK HERE FOR THE CHART!)

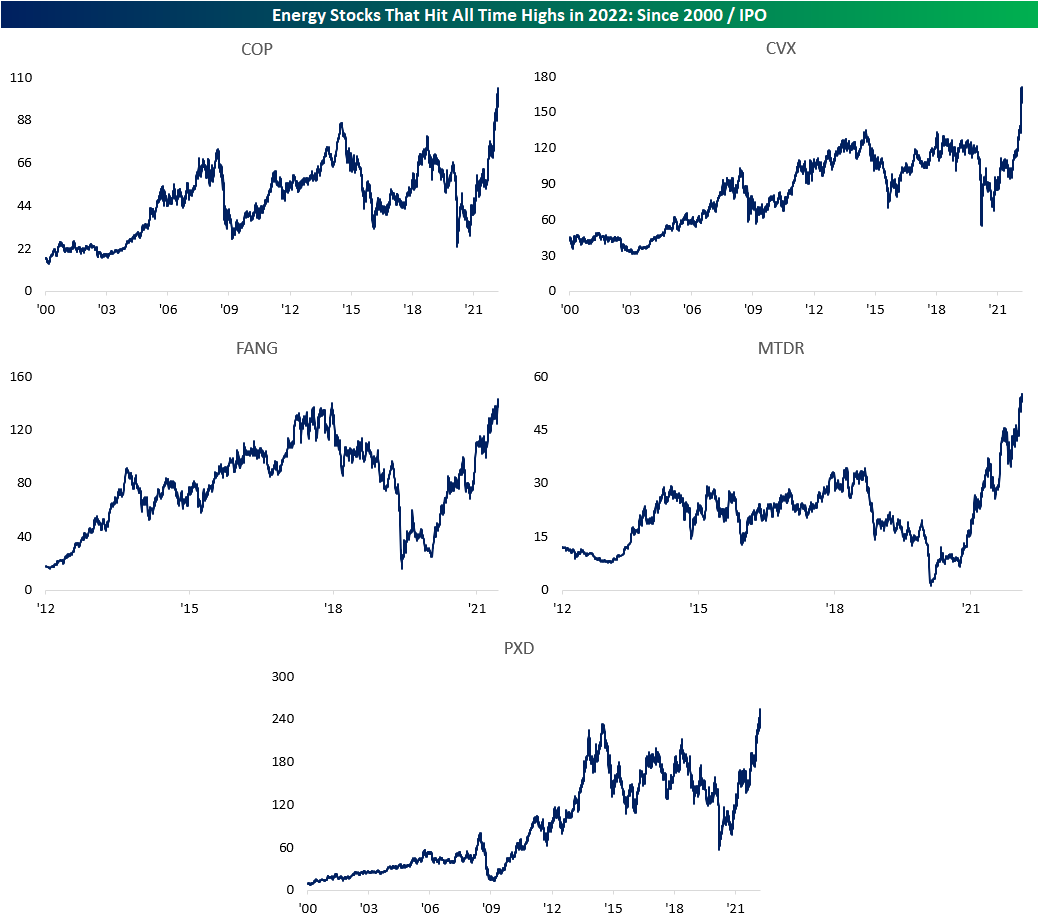

Although Energy has been strong as of late, only five of the 63 Energy sector stocks in the S&P 1500 have hit all time highs in 2022 (to be considered, the stock must have been trading for at least five years). The five stocks are ConocoPhillips (COP), Chevron (CVX), Diamondback Energy (FANG), Matador Resources (MTDR) and Pioneer Natural Resources (PXD). Below are the charts of these stocks since the turn of the century. The average stock on this list is up 41.3% on the year as of yesterday's close, which is only slightly greater than the performance of XLE.

(CLICK HERE FOR THE CHART!)

Not all of the increase to bears came from bulls. As shown below, neutral sentiment fell from 30.2% down to 27.8%. That is only the lowest level since the end of February. While bullish and bearish sentiment are both over a full standard deviation away from their historical averages, neutral sentiment is much more inline with its own historical average. Whereas all weeks since the start of the survey has seen neutral sentiment average a reading of 31.4%, this week's reading was only a few percentage points away.

{kind=link}

{kind=link}

{kind=link}

Bulls and Bears Swing Double Digits

There's nothing like higher prices to cure investor blues, and the last week has been a perfect example of that. AAII's weekly sentiment survey saw a double-digit increase in the percentage of respondents reporting as bullish this week with that reading rising from 22.5% up to 32.8% and matching the highest level of optimism in 2022.

(CLICK HERE FOR THE CHART!)

Those gains to bullish sentiment borrowed entirely from bears as the percentage of respondents reporting as pessimistic fell from nearly 50% of respondents down to 35.4%. The 14.4 percentage point decline marked the largest weekly decline in bearish sentiment since July 2010 when the reading had fallen by 19.27 percentage points. More recently, however, there have been a couple of other double-digit drops in bearish sentiment including a 12.3 percentage point decline in the first week of March and an 11.9 percentage point drop in December.

(CLICK HERE FOR THE CHART!)

Bears continue to outnumber bulls, but the margin has narrowed to the smallest degree since the first week of the year. The bull-bear spread has risen to -2.6 after leaping higher by 24.7 points week over week; the largest one-week increase in the number since October 2019.

(CLICK HERE FOR THE CHART!)

Looking at it another way, this week marked the first time since October 2019 that bullish sentiment rose by at least 10 percentage points while bearish sentiment fell by at least 10 percentage points in the same week. In the table below, we show each prior instance of simultaneous double-digit swings in bullish and bearish sentiment without another occurrence in the previous six months. As for how price action has responded to such swings in sentiment, the S&P 500 has generally seen consistently positive performance in the months ahead, but only one week and one-month performance has been significantly stronger on an average or median basis than what has been the norm.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

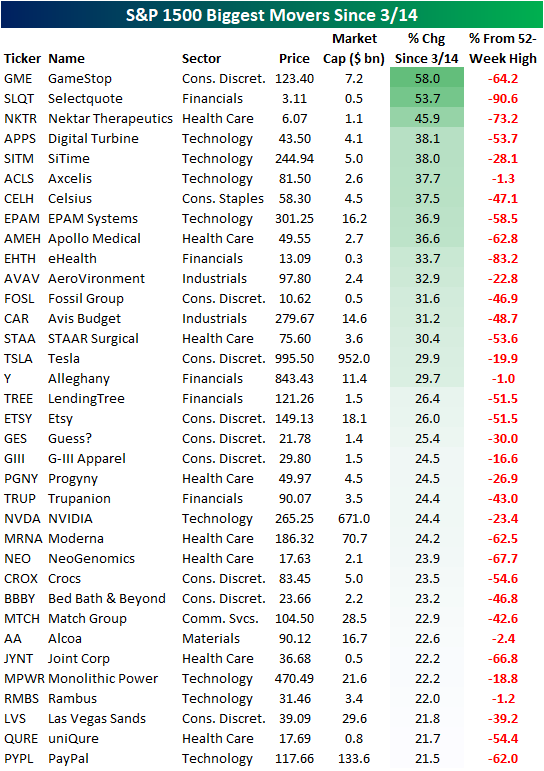

Best Performers Since 3/14 Pivot

Early last week, the US equity market pivoted, gaining 1%+ for four consecutive days between last Tuesday and last Friday (3/15-3/18). Sentiment has shifted amongst the investing community for the time being. For now, it seems that the market may have largely priced in some of the most hawkish Fed tightening scenarios. Remember, we already saw huge drops of 50%, 60%, 70%, even 80%+ in many of the most interest-rate sensitive growth stocks before the Fed even lifted off of 0%. How much further were investors expecting them to go?

Since the 3/14 pivot, certain members of the S&P 1500 have already gained over 20%, but still remain well off of 52-week highs. Of the top 35 performers since last Monday, the average stock is still 43.4% off of its 52-week highs (median: 47.1%). Although there is much recovery room left for many of these high-flyers, this is a move in the right direction. The top performing stock since the 3/14 close is GameStop (GME), which has moved 58.0% higher on the back of a 30.9% move today. This may imply that investors have increased their risk appetite, or that retail investors viewed the dip as a buying opportunity, which would likely apply to the broader market from a retail perspective. Selectquote (SLQT) and Nektar Therapeutics (NKTR) rank immediately below GME, gaining 53.7% and 45.9% respectively. Both of these stocks are operating at a loss on the bottom line, which tells us that the risk-on trade has performed strongly over the last week. Other noteworthy names on the list include Tesla (TSLA), Avis Budget (CAR), Etsy (ETSY), NVIDIA (NVDA) and PayPal (PYPL).

(CLICK HERE FOR THE CHART!)

Breaking this down further, the sectors that help up strongly in the face of a downturn earlier this year have performed the worst since the 3/14 pivot. Utilities and Energy members of the S&P 1500 have only gained 0.6% and 2.6% on average, respectively, since last Monday. On the other hand, Consumer Discretionary, Health Care, and Technology members of the S&P 1500 have gained 7.8%, 8.1% and 10.6% on average, respectively. Based on the data below, the sectors most off their highs have rallied the most aggressively since the pivot, while the sector leaders from pre-3/14 have lagged.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

Best S&P 500 Stocks Since the COVID Crash Lows

Two years ago to the day, the S&P 500 put in a low after a 33.9% pullback from the closing high on 2/19/20. While the S&P 500 is once again off its highs, the index sits just over 100% above that 3/23/20, low and 32.7% above the pre-pandemic high. In the table below, we show the current S&P 500 components which have rallied the most since the COVID Crash low as well as how much each stock declined during the crash.

While it was not a member of the S&P 500 at the time of the COVID crash, being added on 12/21/20, Tesla (TSLA) is currently the S&P 500 member which has risen the most since the broader market low. After being more than cut in half, it has since risen over 1,000%. The next best performers are Devon Energy (DVN) and APA Corp (APA); a couple of Energy sector names that saw even larger declines of 72.8% and 84.86%, respectively from 2/19/20 to 3/23/20. Along since Freeport-McMoRan (FCX), both stocks have risen well over 800% over the past two years. Of the list of the 25 best performers in the S&P 500, the only one that managed to move higher during the COVID Crash was vaccine producer Moderna (MRNA) which had risen 40.43% as the rest of the market collapsed.

(CLICK HERE FOR THE CHART!)

By the time of the 3/23/20 low, the index's worst performers since the pre-pandemic high (2/19/20) had seen monumental declines with many of those stocks dropping over 70%. On the other end of the spectrum, only four stocks had eeked out a gain and only another seven stocks had fallen single-digit percentage points.

As for what those stocks have done since then, below we have created equal weight indices comprised of the S&P 500 members that are still actively traded that were the 20 best and 20 worst performers from 2/19/20 to 3/23/20. Each basket as well as the S&P 500 are indexed to 100 at the COVID Crash low. As shown, what had at one point been the most beaten-down names, have crushed it over the past two years; hypothetically having turned $100 into $481 having even held up well during the recent bout of weakness for equities. For comparison, the biggest winners in the early days of the pandemic bought at the lows would have only seen $100 turn into $137.64 while the S&P 500 as a whole would have a little more than doubled.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

Jobless Claims at Lowest Level in Over 50 Years

Since early December, initial jobless claims have risen and remained above multi-decade lows. That is until this week. Seasonally adjusted claims fell for a second week in a row down to 187K this week. That is the lowest reading since claims came in at 182K all the way back in September 1969.

(CLICK HERE FOR THE CHART!)

While not to take away from the historically strong reading as NSA claims also hit a new low for the pandemic of 181.1K, before seasonal adjustment, jobless claims have not exactly fallen to as significant of a low as the adjusted number. Although that is the lowest level for the current week of the year since 1969, there have been recent periods like the fall of 2018 and 2019 in which claims were even lower. Declines in initial claims have historically been common for the current week of the year, but the next couple of weeks have typically seen claims experience a brief bump before resuming a seasonal downtrend roughly through mid-spring.

(CLICK HERE FOR THE CHART!)

Continuing claims have fallen even more consistently with week-over-week improvements in 7 of the past 10 weeks. Now at 1.35 million, continuing claims are down to the lowest level since the first week of 1970.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

{kind=link}

Here are the most notable companies reporting earnings in this upcoming trading week ahead-

- (T.B.A. THIS WEEKEND.)

([CLICK HERE FOR NEXT WEEK'S MOST NOTABLE EARNINGS RELEASES!]())

(T.B.A. THIS WEEKEND.)

([CLICK HERE FOR NEXT WEEK'S HIGHEST VOLATILITY EARNINGS RELEASES!]())

(T.B.A. THIS WEEKEND.)

Below are some of the notable companies coming out with earnings releases this upcoming trading week ahead which includes the date/time of release & consensus estimates courtesy of Earnings Whispers:

Monday 3.28.22 Before Market Open:

(CLICK HERE FOR MONDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Monday 3.28.22 After Market Close:

(CLICK HERE FOR MONDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK# 1!)

{kind=link}

{kind=link}

Tuesday 3.29.22 Before Market Open:

(CLICK HERE FOR TUESDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Tuesday 3.29.22 After Market Close:

(CLICK HERE FOR TUESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

{kind=link}

Wednesday 3.30.22 Before Market Open:

(CLICK HERE FOR WEDNESDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Wednesday 3.30.22 After Market Close:

(CLICK HERE FOR WEDNESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

{kind=link}

Thursday 3.31.22 Before Market Open:

(CLICK HERE FOR THURSDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Thursday 3.31.22 After Market Close:

(CLICK HERE FOR THURSDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

{kind=link}

Friday 4.1.22 Before Market Open:

([CLICK HERE FOR FRIDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK!]())

(NONE.)

Friday 4.1.22 After Market Close:

([CLICK HERE FOR FRIDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

(NONE.)

DISCUSS!

What are you all watching for in this upcoming trading week?

(T.B.A. THIS WEEKEND.)

(T.B.A. THIS WEEKEND.) (T.B.A. THIS WEEKEND.).

(CLICK HERE FOR THE CHART!)

I hope you all have a wonderful weekend and a great trading week ahead r/stocks🙂

Leave a Reply