Good Friday evening to all of you here on r/stocks! I hope everyone on this sub made out pretty nicely in the market this past week, and are ready for the new trading week ahead. 🙂

Here is everything you need to know to get you ready for the trading week beginning July 25th, 2022.

Markets face what could be the most important week of summer with Fed, earnings and economic data – (Source)

There’s a head-spinning amount of news for markets to navigate in the week ahead, the biggest of which will be the Federal Reserve’s midweek meeting.

The two largest U.S. companies — Microsoft and Apple — report Tuesday and Thursday, respectively. Google parent Alphabet releases results Tuesday, and Amazon reports Thursday. Meta Platforms, formerly Facebook, reports Wednesday. In all, more than a third of the S&P 500 companies are reporting.

On top of that are several hefty economic reports, which should add fuel to the debate on whether the economy is heading toward, or is already in, a recession.

“Next week, I think, is going to be the most important week of the summer between the economic reports coming out, with respect to GDP, the employment cost index and the Fed meeting — and the 175 S&P 500 companies reporting earnings,” said Leo Grohowski, chief investment officer at BNY Mellon Wealth Management.

Second-quarter gross domestic product is expected Thursday. The Fed’s preferred personal consumption expenditures inflation data comes out Friday morning, as does the employment cost index. Home prices and new home sales are reported Tuesday and consumer sentiment is released Friday.

“I think what those bigger companies say about the outlook will be more important than the earnings they post. … When you combine that with the statistical reports, which will be backward looking, I think it’s going to be a volatile and important week,” Grohowski said.

The run-up to the Fed’s meeting on Tuesday and Wednesday has already proven to be dramatic, with traders at one point convinced a full point rate hike was coming. But Fed officials pushed back on that view, and economists widely expect a second three-quarter point hike to follow the one last month.

“Obviously a 75 basis point hike is baked in the cake for next week,” said Grohowski. “I think the question is what happens in September. If the Fed is continuing to stay too tight for too long, we will need to increase our probability of recession, which currently stands at 60% over the next 12 months.” A basis point equals 0.01%.

The Fed’s rate hiking is the most aggressive in decades, and the July meeting comes as investors are trying to determine whether the central bank’s tighter policies have already or will trigger a recession. That makes the economic reports in the week ahead all the more important.

GDP report

Topping the list is that second-quarter GDP, expected to be negative by many forecasters. A contraction would be the second in a row on top of the 1.6% decline in the first quarter. Two negative quarters in a row, when confirming declines in other data, is viewed as the sign of a recession.

The widely watched Atlanta Fed GDP Now was tracking at a decline of 1.6% for the second quarter. According to Dow Jones, a consensus forecast of economists expects a 0.3% increase.

“Who knows? We could get a back-of-the-envelope recession with the next GDP report. There’s a 50/50 chance the GDP report is negative,” Grohowski said. “It’s the simple definition of two down quarters in a row.” He added, however, that would not mean an official recession would be declared by the National Bureau of Economic Research, which considers a number of factors.

Diane Swonk, chief economist at KPMG, expects to see a decline of 1.9%, but added it is not yet a recession because unemployment would need to rise as well, by as much as a half percent.

“That’s two negative quarters in a row, and a lot of people are going to say ‘recession, recession, recession,’ but it’s not a recession yet,” she said. “The consumer slowed quite a bit during the quarter. Trade remains a huge problem and inventories were drained instead of built. What’s interesting is those inventories were drained without a lot of discounting. My suspicion is inventories were ordered at even higher prices.”

Stocks in the past week were higher. The S&P 500 ended the week with a 2.6% gain, and the Nasdaq was up 3.3% as earnings bolstered sentiment.

“We’re really shifting gears in terms of what’s going to be important next week versus this week,” said Art Hogan, chief market strategist at National Securities. “We really had an economic data that was largely ignored. Next week, it will probably equal the attention we pay to the household names that are reporting.”

Better-than-expected earnings?

Companies continued to surprise on the upside in the past week, with 75.5% of the S&P 500 earnings better than expected, according to I/B/E/S data from Refinitiv. Even more impressive is that the growth rate of earnings for the second quarter continued to grow.

As of Friday morning, S&P 500 earnings were expected to grow by 6.2%, based on actual reports and estimates, up from 5.6% a week earlier.

“We have kind of a perfect storm of inputs, pretty deep economic reports across the board, with things that have become important, like consumer confidence and new home sales,” said Hogan “For me, the real tell will be whether the attitude of investors continues to be that the earnings season is better than feared.”

While stocks gained in the past week, bond yields continued to slide, as traders worried about the potential for recession. The benchmark 10-year Treasury yield fell to 2.76% Friday, after weaker PMIs in Europe and the U.S. sent a chilling warning on the economy. Yields move opposite price.

“I do think the market is pivoting,” said Grohowski. “I do think our concerns at least are quickly shifting from persistent inflation to concerns over recession.”

The potential for volatility is high, with markets focused on the Fed, earnings and recession worries. Fed Chair Jerome Powell could also create some waves, if he is more hawkish than expected.

“There are a lot of signs out there about slowing economic growth that will bring down inflation. Hopefully, the Fed doesn’t stay too tight for too long,” said Grohowski. “The chance of a policy error by the Fed continues to increase because we continue to get signs of a rapidly cooling — not just cooling — economy.”

This past week saw the following moves in the S&P:

(CLICK HERE FOR THE FULL S&P TREE MAP FOR THE PAST WEEK!)

{kind=link}

S&P Sectors for this past week:

(CLICK HERE FOR THE S&P SECTORS FOR THE PAST WEEK!)

{kind=link}

Major Indices for this past week:

(CLICK HERE FOR THE MAJOR INDICES FOR THE PAST WEEK!)

{kind=link}

Major Futures Markets as of Friday's close:

(CLICK HERE FOR THE MAJOR FUTURES INDICES AS OF FRIDAY!)

{kind=link}

Economic Calendar for the Week Ahead:

(CLICK HERE FOR THE FULL ECONOMIC CALENDAR FOR THE WEEK AHEAD!)

{kind=link}

Percentage Changes for the Major Indices, WTD, MTD, QTD, YTD as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

S&P Sectors for the Past Week:

(CLICK HERE FOR THE CHART!)

{kind=link}

Major Indices Pullback/Correction Levels as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

Major Indices Rally Levels as of Friday's close:

(CLICK HERE FOR THE CHART!)

{kind=link}

Most Anticipated Earnings Releases for this week:

([CLICK HERE FOR THE CHART!]())

(T.B.A. THIS WEEKEND.)

Here are the upcoming IPO's for this week:

(CLICK HERE FOR THE CHART!)

{kind=link}

Friday's Stock Analyst Upgrades & Downgrades:

(CLICK HERE FOR THE CHART LINK #1!)

{kind=link}

(CLICK HERE FOR THE CHART LINK #2!)

{kind=link}

(CLICK HERE FOR THE CHART LINK #3!)

{kind=link}

August is the worst DJIA and S&P 500 since 1988

August is amongst the worst months of the year. It is the worst DJIA, S&P 500, Russell 1000 and Russell 2000 month over the last 34 years, 1988-2021 with average declines ranging from –0.3% by Russell 2000 to –0.8% by DJIA. For NASDAQ August ranks second worst over the same period with an average gain of 0.3%.

(CLICK HERE FOR THE CHART!)

Contributing to this poor performance since 1988; the second shortest bear market in history (45 days) caused by turmoil in Russia, the Asian currency crisis and the Long-Term Capital Management hedge fund debacle ending August 31, 1998, with the DJIA shedding 6.4% that day. DJIA dropped 1344.22 points for the month, off 15.1%—which is the second worst monthly percentage DJIA loss since 1950. Saddam Hussein triggered a 10.0% slide in August 1990. The best DJIA gains occurred in 1982 (11.5%) and 1984 (9.8%) as bear markets ended. Sizeable losses in 2010, 2011, 2013 and 2015 of over 4% on DJIA have widened Augusts’ average decline.

(CLICK HERE FOR THE CHART!)

In midterm years since 1950, Augusts’ rankings improve slightly: #8 DJIA and S&P 500, #10 NASDAQ (since 1974), #5 Russell 1000 and #10 Russell 2000 (since 1982). Average losses range from –0.2% for S&P 500 to –1.3% for Russell 2000. Russell 1000 has advanced 0.2% on average in midterm Augusts. All five indexes having winning track records, but losses have frequently been substantially larger than gains. DJIA and NASDAQ suffered double-digit losses in 1974, 1990 and 1998.

{kind=link}

{kind=link}

Third Longest Streak of Negative Bull-Bear Spread on Record

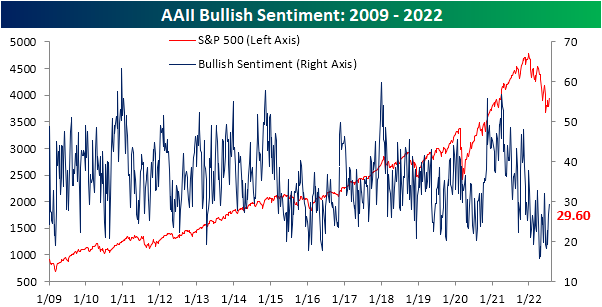

Last week, over a quarter of respondents to the AAII sentiment survey reported bullish sentiment for the first time in over a month. As the S&P 500 has made a considerable move to the upside, bulls have continued to come back this week rising to 29.6%. The percentage of respondents reporting as optimistic has now come back within one standard deviation of its historical average and is at the highest level since the first week of June.

(CLICK HERE FOR THE CHART!)

Bearish sentiment has fallen in lockstep with the increase in bullish sentiment. After coming in at over 50% two weeks ago, the reading has shed 10.6 percentage points. Albeit improved, bearish sentiment remains well above the historical average and the double-digit two-week decline is actually the seventh of the year. In other words, the sharp drop in bearish sentiment is not exactly unusual compared to other moves this year as it still has further to go until it reaches a more “normal” level.

(CLICK HERE FOR THE CHART!)

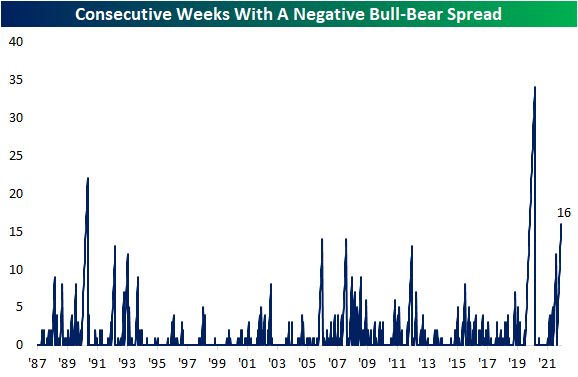

Regardless, with inverse moves in bulls and bears the bull-bear spread has risen to -12.6. That is the highest reading since the first week of June and, as shown in the second chart below, the 16th consecutive week with bears outnumbering bulls. Clearing two other streaks from the early 2000s, that is now the third longest streak on record behind the 22 and 34-week-long streaks ending in December 1990 and October 2020, respectively.

(CLICK HERE FOR THE CHART!)

(CLICK HERE FOR THE CHART!)

Not all of the losses to bears went to bulls. Neutral sentiment also rose this week rising to 28.2% from 26.6% last week. That is the highest level in three weeks as neutral sentiment has generally been less volatile than bulls and bears recently.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Declines Abound in Mortgage Data

Roughly one month ago, the national average for a 30 year fixed rate mortgage peaked above 6%. Since then, the rate has pulled back and stabilized around 5.75% in the past several weeks. Although mortgage rates have stabilized a bit, they remain at some of the highest levels since 2008 and have been heading marginally higher in the past week.

(CLICK HERE FOR THE CHART!)

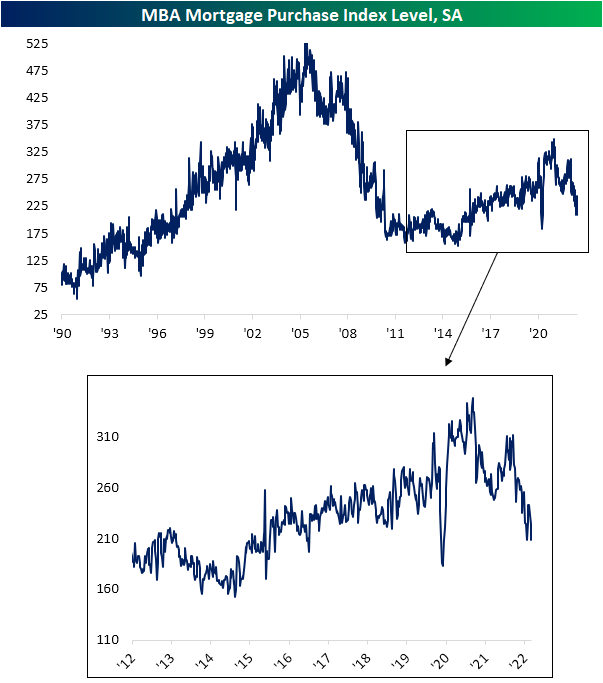

Given the slight rise in rates, demand for mortgages continues to predict further weakness in upcoming home sales data as we noted in today's Morning Lineup. The MBA's Mortgage Purchase index released this morning came in at a slightly lower reading than the June 3rd low for the weakest reading in the index since March and April of 2020. This week's low is also below the range from the few years prior to the pandemic.

(CLICK HERE FOR THE CHART!)

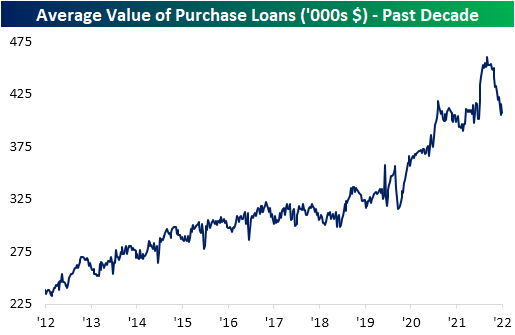

Not only has there been a lower volume of mortgages being applied for, but the actual dollar value of those loans has also plummeted amidst higher rates. As shown below, the average value of purchases reached a high of $460K back in March after a big increase in the first few months of this year. Since then, it has entirely reversed that move with the average value of loans having fallen all the way back down to $406K. That echoes the findings in other recent housing data which has similarly shown declines in home prices.

(CLICK HERE FOR THE CHART!)

Higher rates have had an even more significant impact on refinance activity. Following another drop this week, the MBA's index tracking refinancings has now reached the lowest level since November 2000.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

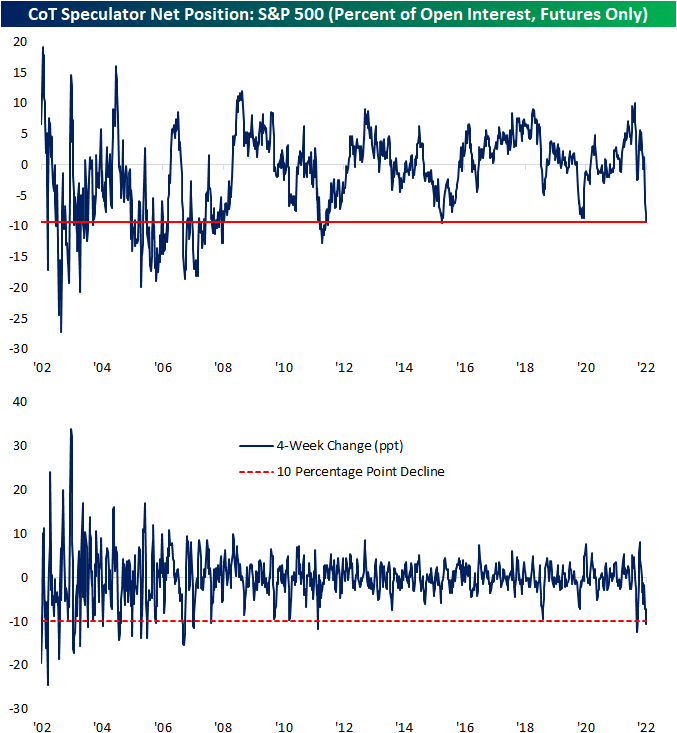

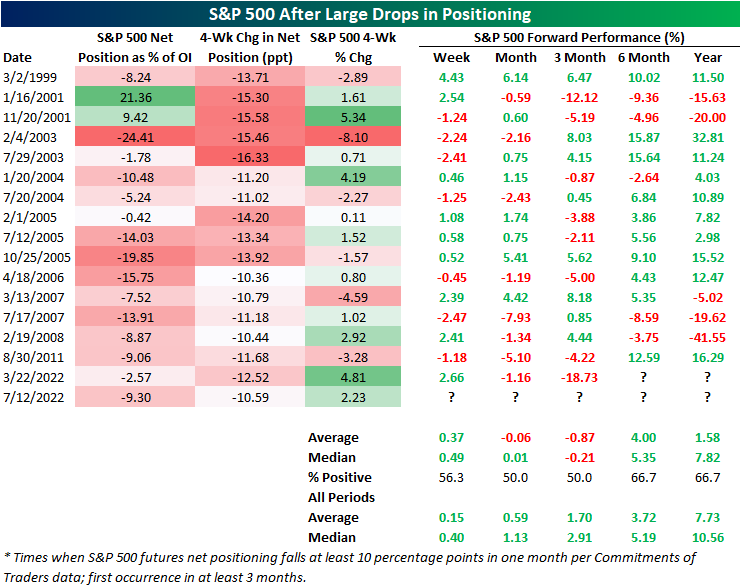

Speculators Head for the Hills

As we do each Monday in our Closer report, we reviewed the latest data from Friday's release of the CFTC's Commitments of Traders (CoT) Report. This data shows how speculators are positioned in various assets based on positions in the various futures contracts. One asset that has seen some of the most notable changes of the report in recent weeks has been the S&P 500. As recently as one month ago, that data showed a net 1.29% of open interest was positioned long. Even though the S&P 500 has managed to come off the lows in the past month, positioning has collapsed with a massive move lower meaning there are far more speculators positioned short than long.

Whereas one month ago the reading was net long, in the latest data as of last Tuesday a net 9.3% of open interest was short. That made for the lowest reading since October 2015. In other words, speculators are positioned more pessimistically now than they were during the COVID crash, during the late 2018 near bear market, or any other time over the past several years. The change in positioning has also been rapid. As shown in the second chart below, that net positioning reading has fallen over 10 percentage points in just 4 weeks. Earlier this year in March there was an even larger 12.5 percentage point decline but prior to that, looking back through the history of this data, such large moves have been much rarer over the past decade than was the case in the 2000s and before. In fact, prior to this year the last time positioning in S&P 500 futures fell double digits in four weeks was all the way back in August 2011. On the other hand, the early 2000s frequently saw moves of this size if not larger.

(CLICK HERE FOR THE CHART!)

Typically, sentiment data is considered contrarian in nature. In other words, pessimistic sentiment readings are followed by stronger forward performance of equities and vice versa. That has not exactly been the case for this CoT positioning data. Following past declines of at least 10 percentage points, returns have been mixed.

After declines of similar magnitude, the S&P 500 has experienced modest outperformance over the next week. One and three months out, however, have tended to be weaker with postive returns only half the time with negative returns on an average basis. Over the next month, each of the past four instances have been followed by declines.

Six and twelve months out have seen the S&P 500 higher two-thirds of the time, but average and median returns are not significantly better relative to all periods.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

More Small-cap weakness likely as Russell 2000 enters historically weakest part of year

(CLICK HERE FOR THE CHART!)

In the above chart, 43 years of daily data for the Russell 2000 index of smaller companies are divided by the Russell 1000 index of largest companies, and then compressed into a single year to show an idealized yearly pattern. When the graph is descending, large caps are outperforming smaller companies; when the graph is rising, smaller companies are moving up faster than their larger brethren. Small-caps have historically peaked versus large-caps in late-May to early June and tend to underperform until sometime in the fourth quarter.

{kind=link}

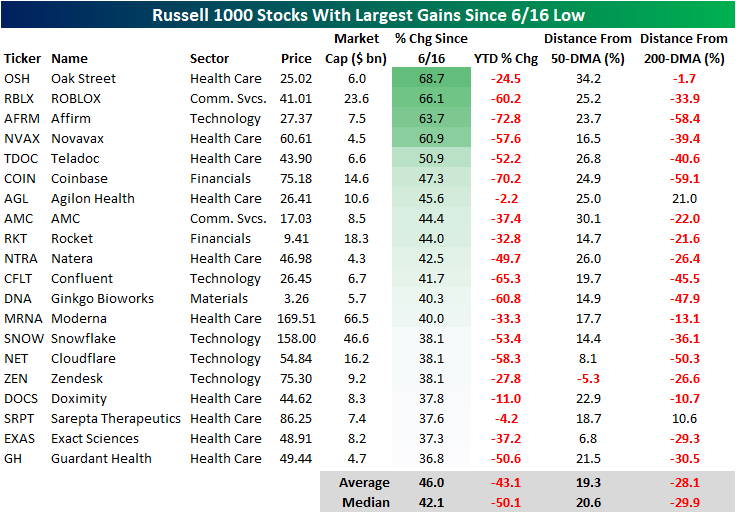

Best Performers Since Mid-June Low

Since June 16th, the market has reversed course higher, making the date at least a near-term bottom. From a technical perspective, the Russell 1000 broke through its 50-day moving average yesterday and broke above its upper downtrend line today. The 50-DMA is still moving lower, but this is the first time that the Russell 1000 has been above the 50-DMA since April 20th. However, the index is still 9.7% below its 200-DMA. These moves come as commodity prices have pulled back and earnings season begins.

(CLICK HERE FOR THE CHART!)

As we highlighted in a Chart of the Day earlier this week, the lagging sectors during bear market declines tend to be the leaders in bear market rallies, which is holding true in the bounce since 6/16. The table below shows the 20 best performing stocks in the Russell 1000 Index since the 6/16 low. As you can see, these stocks are all still down considerably on a YTD basis, declining a median of 50.1%. However, these stocks have rebounded by a median of 42.1% since the low on 6/16. Only one of these stocks is below its 50-DMA, and only two are above their respective 200-DMA. If you think that the bear market has concluded, these would be some of the names worth looking deeper into.

(CLICK HERE FOR THE CHART!)

On the other hand, the best performing sectors during bear market declines tend to be the worst performing sectors during bear market rallies. Of the 20 worst performing Russell 1000 stocks since 6/16, 14 belong to the energy sector (which has been the best sector on a YTD basis by a wide margin). On a median basis, these 20 stocks are still up 13.6% on a YTD basis, but they've shed 13.7% of their value since the market bottomed in mid June. Notably, these stocks (on a median basis) are closer to their 200-DMAs than they are to their 50-DMAs. If you think that we are currently in a bear market rally that is bound to reverse course, these names would be worth looking deeper into.

(CLICK HERE FOR THE CHART!)

{kind=link}

{kind=link}

{kind=link}

(CLICK HERE FOR THE CHART!)

{kind=link}

Here are the most notable companies (stock tickers) reporting earnings in this upcoming trading week ahead-

- ((T.B.A. THIS WEEKEND.))

([CLICK HERE FOR NEXT WEEK'S MOST NOTABLE EARNINGS RELEASES!]())

(T.B.A. THIS WEEKEND.)

(CLICK HERE FOR NEXT WEEK'S HIGHEST VOLATILITY EARNINGS RELEASES!)

{kind=link}

(CLICK HERE FOR THE MOST NOTABLE EARNINGS RELEASES FOR THE NEXT 3 WEEKS!)

{kind=link}

Below are some of the notable companies coming out with earnings releases this upcoming trading week ahead which includes the date/time of release & consensus estimates courtesy of Earnings Whispers:

Monday 7.25.22 Before Market Open:

(CLICK HERE FOR MONDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Monday 7.25.22 After Market Close:

(CLICK HERE FOR MONDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

{kind=link}

Tuesday 7.26.22 Before Market Open:

(CLICK HERE FOR TUESDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

Tuesday 7.26.22 After Market Close:

(CLICK HERE FOR TUESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #1!)

(CLICK HERE FOR TUESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #2!)

{kind=link}

{kind=link}

{kind=link}

Wednesday 7.27.22 Before Market Open:

(CLICK HERE FOR WEDNESDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK #1!)

(CLICK HERE FOR WEDNESDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK #2!)

Wednesday 7.27.22 After Market Close:

(CLICK HERE FOR WEDNESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #1!)

(CLICK HERE FOR WEDNESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #2!)

(CLICK HERE FOR WEDNESDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #3!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Thursday 7.28.22 Before Market Open:

(CLICK HERE FOR THURSDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK #1!)

(CLICK HERE FOR THURSDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK #2!)

(CLICK HERE FOR THURSDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES LINK #3!)

Thursday 7.28.22 After Market Close:

(CLICK HERE FOR THURSDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #1!)

(CLICK HERE FOR THURSDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #2!)

(CLICK HERE FOR THURSDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES LINK #3!)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Friday 7.29.22 Before Market Open:

(CLICK HERE FOR FRIDAY'S PRE-MARKET EARNINGS TIME & ESTIMATES!)

{kind=link}

Friday 7.29.22 After Market Close:

([CLICK HERE FOR FRIDAY'S AFTER-MARKET EARNINGS TIME & ESTIMATES!]())

(NONE.)

(T.B.A. THIS WEEKEND.)

(T.B.A. THIS WEEKEND.) (T.B.A. THIS WEEKEND.).

(CLICK HERE FOR THE CHART!)

DISCUSS!

What are you all watching for in this upcoming trading week?

I hope you all have a wonderful weekend and a great trading week ahead r/stocks. 🙂

Leave a Reply